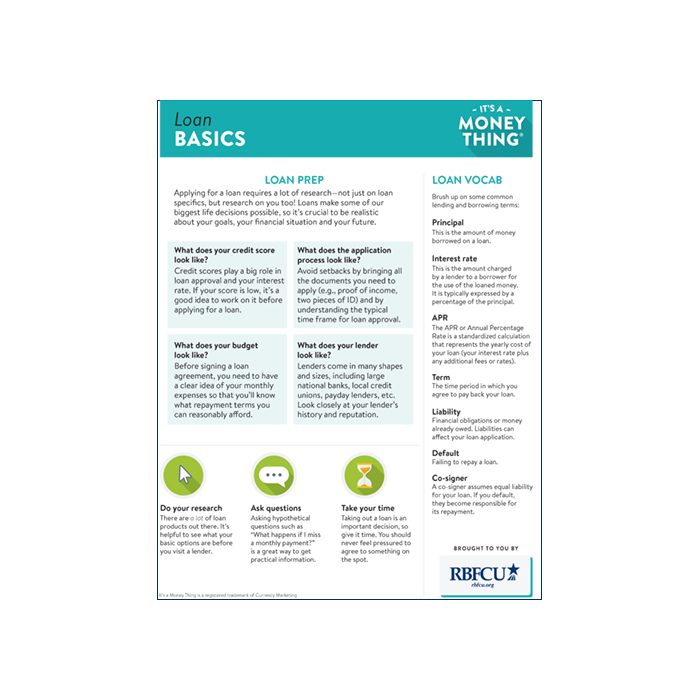

3 Tips to Help You Make a Smart Loan Decision

If you’re not able to make a large purchase with the money available in your savings account, don’t feel bad. Most people aren’t able to buy a car or home without borrowing money from a credit union or bank, which is why auto loans and mortgage loans exist.

However, taking out a loan isn’t to be taken lightly. It’s easily one of the biggest monetary decisions you’ll make in life. Here are three ways to make sure you get the best loan for your budget, and that you’re able to pay it back.

Tip #1: Look around

Before taking a loan, shop around. Try to find the best interest rate, the best loan terms, the lowest fees and the best repayment options.

If it’s your first time taking out a loan, learn more about how a loan works. Most loans will either have a fixed rate or an adjustable rate. A fixed-rate loan may have a higher interest rate, but the payments will be consistent, and easier to budget for. An adjustable-rate loan may offer a lower interest rate to start, but your monthly payments might increase as the interest rate fluctuates.

Tip #2: Figure out how much you should borrow

Do your homework and figure out how much can afford to budget for a loan payment each month. And don’t forget that the purchasing power of a loan often leads to other new expenses.

For example, if you’re purchasing a car or home, you’ll also need to budget for expenses like insurance and maintenance. A home has even more added costs, like property taxes, homeowners association fees and utilities.

A good rule of thumb is to aim to limit your housing and related expenses to 30 percent of your monthly budget.

Tip #3: Make a plan

Don’t rush into a loan; you should never borrow in the moment. Always take some time to think and assess.

Make a solid plan to pay back your loan in full, that includes all your current expenses, as well as any additional expenses you’ll be taking on to supplement your home or auto purchase. You’ll also need to account for any extra expenses you might run into; an emergency fund can help with those. If you have extra money in your budget, consider using it to make additional loan payments whenever possible, which will help you save on your total interest over the life of the loan.

Ideally, a loan should serve to improve your overall financial situation, not hurt it. If you shop around, borrow a reasonable amount and make a plan, you’ll be on your way to making a smart decision when you take out a loan.