Responding to Financial Emergencies in Times of Uncertainty

The COVID-19 pandemic is a sobering reminder that financial challenges come in all shapes and sizes. Some obstacles — such as job loss or income reduction — are immediate and obvious.

Others — such as fear or uncertainty about the future — are more subtle, but they can still disrupt our regular spending and saving patterns in a negative way.

Although there isn’t a one-size-fits-all solution to financial emergencies, there are steps you can take that will minimize damage while you work on a recovery plan. When confronted with a financial emergency, consider doing the following:

Step #1: Stop the Bleeding

Immediately limit your spending to essentials only — at least until you figure out how much money you need in order to recover from your emergency. In this case, an essential expense is any purchase that keeps you productive while you tackle your obstacles. Protect your ability to eat, sleep and to continue to earn income. Pause, skip or cancel everything else.

(Article continues below video)

It may seem punishingly frugal at first, but every dollar you save gets you one step closer to recovery. Continuing to spend money as you normally do can sabotage your efforts to get back on track.

Entertainment expenses (think streaming services, gaming subscriptions and app memberships) are a good place to start cutting costs, since they are easy to pause or cancel online.

Step #2: Take a Close Look at What’s Going On

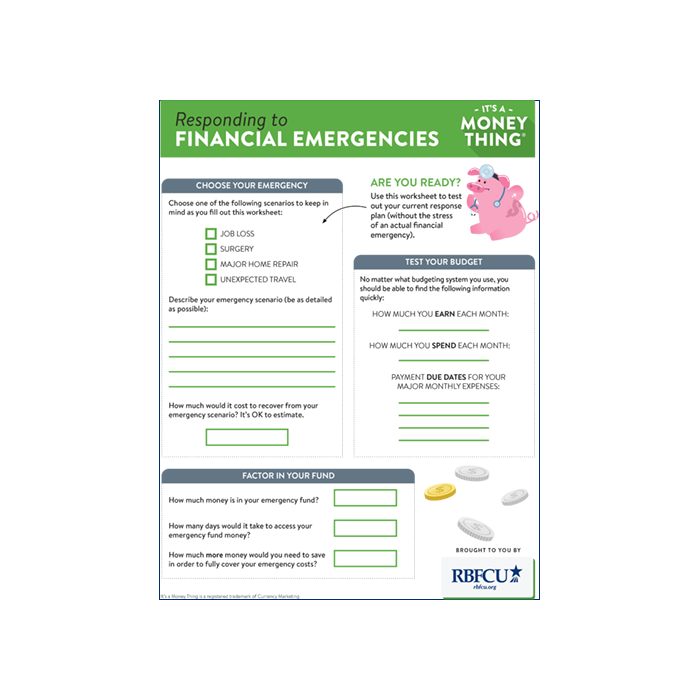

Take the time to calculate the total financial impact your emergency will have on your budget. This includes the cost of the emergency itself, plus any costs resulting from its consequences. A hefty medical bill is an example of an emergency expense; the additional cost of carrying debt resulting from that bill is an example of a consequence. The more realistic and accurate you are with your calculation, the more effective your recovery plan will be.

Reducing your spending, consulting your budget, extending your payment due dates and seeking support will help ease the road to recovery when dealing with a financial emergency.

Consulting your budget is another crucial part of this step. If you don’t have a budget in place, create one. Use any method you prefer — app, spreadsheet, pen and paper — as long as you are able to accurately capture how much you earn and spend each month. This will help inform your recovery plan: You’ll know how much money you’re able to contribute each month and roughly how long it will take to recover.

Step #3: Put a Band-aid on the Situation

When dealing with a financial emergency, look for temporary solutions that will help keep things manageable while you seek the appropriate help. In some cases, moving your payment due dates can ease some of the stress — especially if several of your payment dates are close together. Call your financial institution, your credit card company and your utility company to explain the situation and to see if you can reschedule a payment date without penalty. Doing so helps prevent your emergency from setting off a domino chain of late fees and missed payments.

Step #4: Seek the Appropriate Help

It’s normal to feel helpless and alone in emergency circumstances, which is why it’s especially important to seek out knowledgeable guidance in times of financial stress. Aid can come in many forms, including financial relief, education, counseling and support. Research resources offered through your financial institution, through government programs and through other organizations. Your credit union may have access to additional resources you are not already aware of.

Reducing your spending, consulting your budget, extending your payment due dates and seeking support will help ease the road to recovery when dealing with a financial emergency. Whether you need to replace income or cover an unexpected expense, the four steps listed above will help you evaluate the problem and deal with it in a smart and efficient way.